What is a Mortgage Contingency? Deadlines, Risks, and Best Practices

April 23, 2026

Advantages of FHA Loans: An Affordable Path to Homeownership

May 28, 2026

You’ve probably heard your lender review your “cash to close”, but what is it? Your cash to close is the money you need to provide on closing day. For many first-time buyers, that number can feel higher than expected because it includes more than they think.

Cash to close usually includes your down payment, closing costs, prepaid expenses, and escrow funding. It may also be modified by credits or deposits you have already paid, such as earnest money.

Once you understand how the number is calculated, it becomes easier to review your estimate, plan your budget, and feel more prepared before closing day.

| Looking to Buy This Summer? Start today by getting pre-approved. It’s quick and hassle free. Give us a call at 1-866-532-0550 to learn more or get preapproved today with our easy-to-use digital preapproval app. With Pro SNAP, getting approved is secure, convenient, and takes as little as 15 minutes. |

What Does Cash to Close Mean?

Cash to close is the total amount a buyer must provide to complete the home purchase. It is the final number shown on your Closing Disclosure. This is not a single cost, but rather a combination of several expenses minus any credits or funds you have already paid.

A simple way to think about it is:

Cash to close = down payment + closing costs + prepaids and escrow deposits – credits and deposits already paid

What is Included in Cash to Close?

Here is a quick snapshot of how each expense can change your final amount:

| Cost Type | What it Covers | Increase or Reduction |

| Down Payment | Part of the purchase price you pay upfront | Increase |

| Closing Costs | Lender, title, appraisal, recording, and third-party fees | Increase |

| Prepaids and Escrow Deposits | Taxes, insurance, prepaid interest, and escrow fees | Increase |

| Credits and Deposits | Seller credits, lender credits, and earnest money already paid | Reduction |

How Does the Down Payment Affect Cash to Close?

Your down payment is usually one of the largest contributions toward closing. The down payment amount depends on your loan program and the amount you choose or are required to put down. Because of that, and other factors, two buyers purchasing homes at the same price may have different cash-to-close amounts.

What Closing Costs Are Included in Cash to Close?

Closing costs are the charges tied to creating the loan and transferring the property. Some come from the lender, while others go to outside companies or local offices.

Common closing costs may include:

- Loan origination fees

- Underwriting fees

- Appraisal fee

- Credit report fee

- Title services

- Recording fees

- Escrow or settlement charges

Each fee may look manageable on its own. Together, they can add several thousand dollars to your cash to close. You’ll usually see the costs listed on your Loan Estimate early in the process and on the final Closing Disclosure near your close date.

What Are Prepaids and Escrow Deposits?

Prepaids are upfront homeownership expenses that are collected at closing. They are not the same as lender fees. Instead, they help cover certain bills that are due right away.

Prepaid costs and escrow deposits may include:

- The first year of homeowners’ insurance

- Property taxes due at or near closing

- Prepaid interest from your closing date to the start of your first full mortgage payment period

- A few months of taxes and insurance if your lender sets up an escrow account

How Credits and Earnest Money Can Lower Cash to Close

Credits and deposits can reduce the amount of money you need to bring to closing. This is one of the most important parts that can impact your final number.

Common items that may reduce cash to close include:

- Earnest money deposit: Money you already paid after your offer was accepted. This is typically credited toward your final amount at closing.

- Seller credits: Money the seller agrees to contribute toward eligible closing costs or prepaid expenses.

- Lender credits: Money the lender applies toward closing costs, often in exchange for a higher interest rate.

- Other adjustments: Certain prorations or credits may be added depending on taxes, fees, or timing.

Credits can help lower your out-of-pocket costs, but they do not always apply to every part of the cash to close.

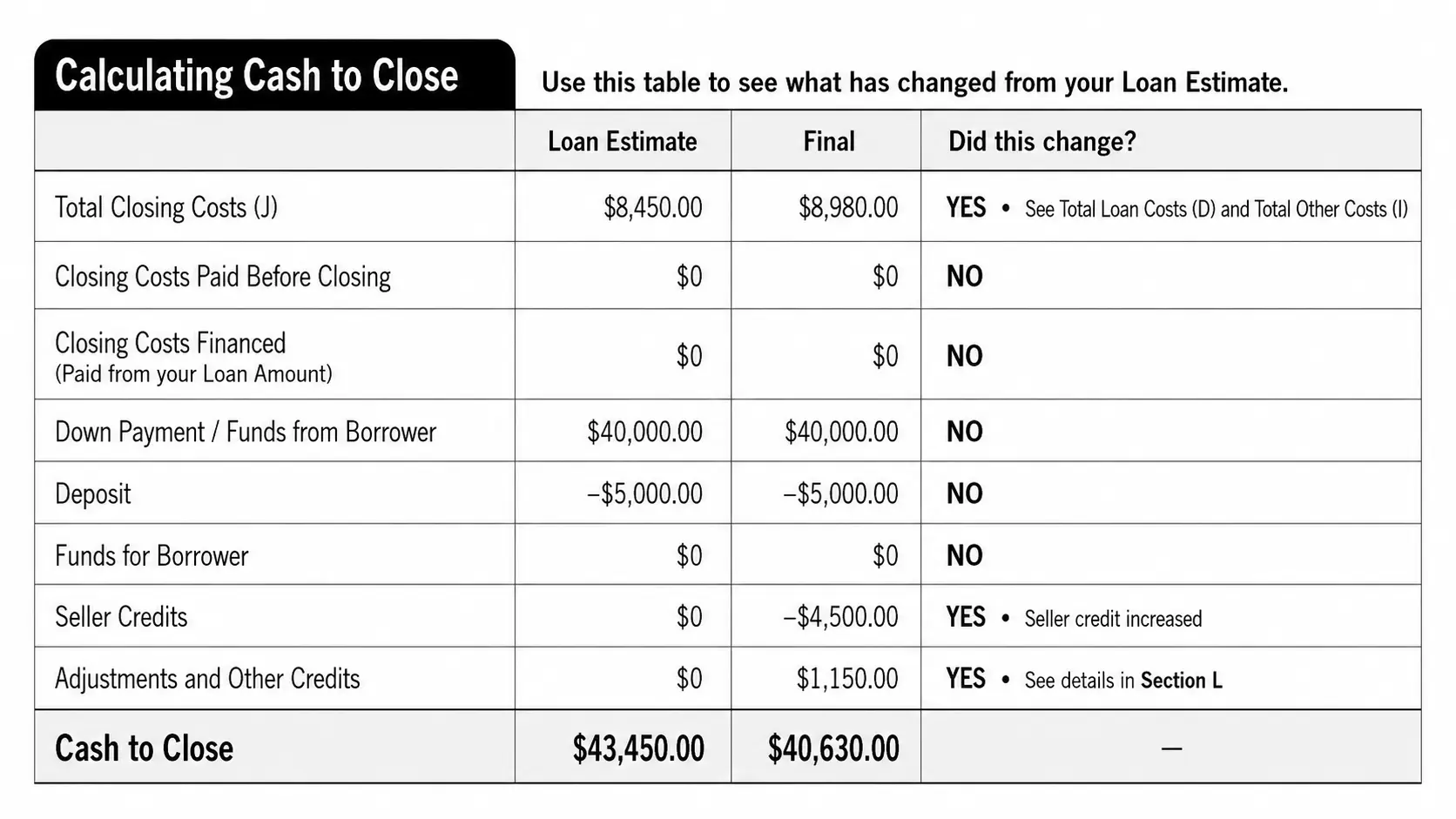

Where Can You Find Your Cash to Close Amount?

You can find your estimated cash to close on your Loan Estimate, which is provided early in the mortgage process. Before closing, you will receive a Closing Disclosure with your updated final amount.

It is normal for your cash to close to change during the loan process. Your amount may shift if your purchase price, interest rate, closing date, homeowners’ insurance, property taxes, seller or lender credits, or final title and recording fees change.

When reviewing these documents, look closely at:

- Estimated cash to close

- Total closing costs

- Down payment amount

- Prepaid taxes and insurance

- Escrow deposits

- Seller credits

- Lender credits

- Earnest money deposit already paid

If the amount is very different from what you expected, ask your loan officer to walk through the numbers with you before closing day.

How Do You Pay Cash to Close?

Buyers usually pay their cash to close with a wire transfer or certified funds, such as a cashier’s check. The title company or closing agent will provide instructions before closing.

Before sending money, always confirm the payment instructions directly with your title company, closing agent, or lender using a trusted phone number. This is especially important if you receive wiring instructions by email, because wire fraud can happen during real estate transactions.

In most cases, personal checks are not accepted for large closing amounts. Your closing team will let you know the approved payment method and when the funds are due.

Get a Clearer Picture of Your Cash to Close

Cash to close can feel overwhelming when you only see the final number. But once you understand what goes into it, including your down payment, closing costs, prepaids, and possible credits, it becomes much easier to plan ahead.

At Mortgage 1, our loan officers can walk you through your estimate, explain what each cost means, and help you understand your mortgage options before closing day arrives. If you are preparing to buy a home, contact Mortgage 1 to get started with confidence.

Common FAQs About Cash to Close

Cash to close is the total amount of money you need to bring on closing day. It usually includes your down payment, closing costs, prepaid expenses, and escrow funding, minus any eligible seller or lender credits.

No. Closing costs are only one part of your cash to close. Your total cash to close may also include your down payment, prepaid taxes, homeowners’ insurance, prepaid interest, and money needed to set up an escrow account.

Your cash to close can change if your purchase price, interest rate, closing date, taxes, insurance, or credits change during the loan process. Review your Loan Estimate and Closing Disclosure carefully, and ask your loan officer about anything that looks different.