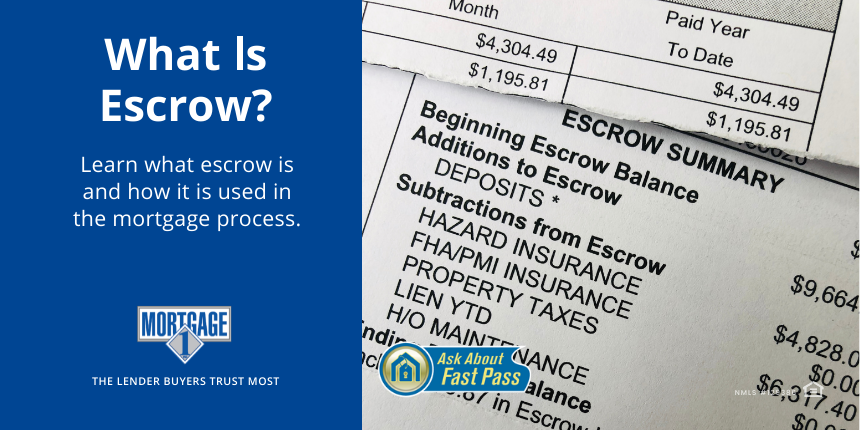

What Is Escrow? How Does It Work?

April 14, 2022

The Benefits of Paying Off Your Home Loan Early

April 28, 2022

Did you know that a home loan can reduce your tax payments? Depending on how you use the property, you may be eligible for a federal tax deduction.

Home ownership comes with a lot of expenses, some of them unexpected. Finding out that you may be able to deduct several thousand dollars sounds appealing, right? So why don’t more homeowners take advantage of this deduction?

In this article, we’ll give you an overview of the mortgage interest deduction on your federal taxes.

| Know Your Mortgage Options Mortgage 1 has helped thousands of people find the home loan that works best for them. Call us at 1-866-532-0550 or use our Pro SNAP digital app to get started. |

What Is a Mortgage Interest Deduction?

Your monthly mortgage payment is divided into several parts, including the principal (i.e. the mortgage amount owing) and the interest you pay to the lender. (Depending on the terms of your mortgage, you might also have private mortgage insurance, homeowners’ insurance, property taxes, and other items included in your monthly payment, but they don’t concern us right now.)

The interest you pay each year can be deductible on your U.S. federal tax return – but only if you meet certain requirements.

| It’s important to note that you can’t deduct the amount paid towards the loan principal– just the amount that goes towards the loan interest. Also be sure to consult your tax advisor regarding your specific circumstance. |

Factors that Influence Your Mortgage Interest Deduction

Calculating the deduction for your mortgage interest can be complicated; of course, the primary factor in the amount you claim is the amount of interest you’ve paid over the tax year. Bankrate’s Mortgage Interest Deduction Calculator can give you an idea of the math you’ll need to do.

The type of deduction you claim on your federal income tax determines if you use your mortgage interest deduction. If you use a standard deduction, you can’t deduct your mortgage interest. On the other hand, if you itemize your deductions and your loan meets the requirements, the deduction is yours to claim.

What affects your eligibility? There are many factors; we recommend consulting a tax professional to get customized advice. However, the general rule is that:

- You must use the loan to purchase your home or make improvements to your primary residence.

- Loans used for second homes or vacation homes may also be eligible.

- You can only count the interest paid on the first $750,000 of the loan. Older loans (taken out before December 2017) may have a higher cutoff.

Why Some People Don’t Claim a Mortgage Interest Deduction

Why might you not take this deduction? If your standard deduction is greater than your itemized deductions, you can’t add the mortgage interest deduction to your standard deduction; you’d have to choose one. And in that case, you’d choose the standard deduction.

Need Help Optimizing Your Mortgage Options?

Mortgages (and taxes!) are complicated and confusing. If you need help figuring out a better home loan solution, contact the Mortgage 1 team today! You can get started by calling 1-866-532-0550 or using our Pro SNAP digital mortgage tool.